Consumers are plagued by soaring prices, empty shelves, and hard-to-find items since the COVID-19 pandemic interrupted supply chains. Families, with limited income, experienced the fiercest struggles, often depleting savings, borrowing money, or tapping retirement funds. Many are penny-pinching, even dangerously reducing vital medicines and food to survive. Others cannot afford high-interest, hard-to-find homes and cars! The Pew Foundation recently reported 72% of respondents were stressed about food and consumer prices. Yet, according to several studies, USA Today reports an average American adult spends $18,000 annually on “non-essential” items. Does Starbucks ring a bell?

March 2024 Consumer-Price-Index-Inflation-Rate is 3%. Surprisingly, inflation formulas exclude volatile items that impact consumers the most—fuel and food. Companies are skillfully raising prices while providing customers with less. Potato chip bags filled with air to appear loaded are only half-full when opened. Our cat litter’s price nearly doubled and weights were cleverly reduced from 10-to-7 pounds. Yet, identical-looking packaging fooled me! Walmart, Home Depot, and Coca-Cola CEOs report that while prices were falling towards the Federal Reserve’s inflation 2% target, “many high-costs remain stuck.” Let’s begin with broad saving suggestions, but keep in mind that percentages may vary by family.

Play “saving” like fun games: While it’s unrealistic to employ in all circumstances, strive to “reasonably” avoid paying retail prices. However, you don’t want saving money to become an unhappy obsession. It’s thrilling to find good deals but remember “you get what you pay for!” There are three distinct categories of savers: (1) savvy, (2) frugal, and (3) cheap (which robs you of having fun and can result in inferior purchases).

Be patient: Successful financial stewards avoid falling into impulsive high-price spending but seek sales and discounts. Webster defines “Patience is the ability to wait for something without frustration. It’s a useful skill and a virtue of one’s personality.”

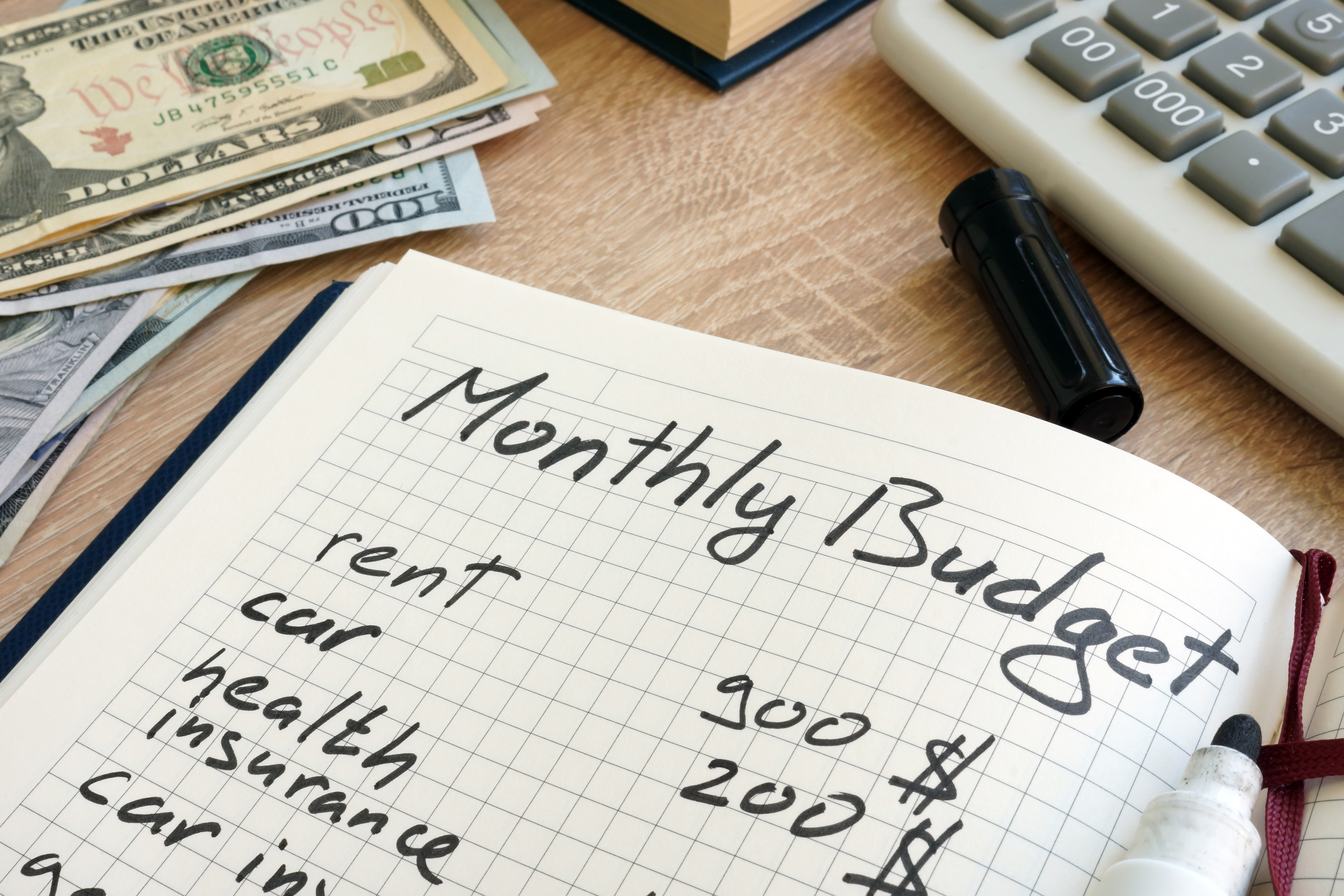

Develop budgets: These roadmaps will productively keep you financially on track and reveal dangers. Gallup Polls determined 66% of families don’t have budgets to guide them and 47% of businesses operate in the dark without financial plans. As Yogi Berra counsels, “If you don’t know where you are going, you might not get there!”

Many families and companies base their expenses and revenue on “unrealistic hopes and dreams!” Households don’t include “unexpected” job losses, disabilities, accidents, deaths, and major expenses. Businesses without cash reserves often are unprepared for disasters like pandemics, competitors attracting lucrative customers, and key employees exiting, which devastate cash flow and earnings. Many fail to “Hope for the best and plan for the worst!”

It’s important to create accurate pictures of your current finances in planning future needs. Carefully examine checkbooks, bank/credit statements, and debit/cash receipts for three months to create your budget. You will be surprised to find that 25-35% of expenses could be miscellaneous! It’s those small expenditures that add to the bigger picture. Some outlays vary with utilities higher in the summer/winter. Adopt the budget philosophy of calculating conservative income combined with liberal, miscellaneous, and unexpected expenses.

Once budgets are developed, crosscheck upcoming “actual” monthly expenses against your “projections” to factually track spending and pinpoint hemorrhaging areas. If developed properly, your strengths and opportunities for improved savings will emerge.

Live within your means: If you don’t have the funds in your budget, delay or avoid buying items. The Bible and Aristotle warn about worshipping money and undisciplined overspending. I traveled down these harmful paths but fortunately realized the dangers after years of running on senseless money-making treadmills. Haven’t we all fallen prey lusting for something we can do without and impatiently wanting it…NOW? Luring, easy-to-obtain credit cards with sky-high interest rates, 10-year car loans, and second-third home mortgages make it possible to buy about anything we desire, especially if trying to keep up with others’ lifestyles. Financial advisor Dave Ramsey noted, “Many families recklessly spend money they don’t have, on things they don’t need, to impress people they don’t like!”

Strive to be debt-free: This takes carefully-designed plans and often third-party professional help to rid yourself of expensive, monthly payments with high-interest rates! Secure 15-year versus 30-year home mortgages to save bundles on interest or frequently pay extra towards your existing loan’s principal. If credit cards hold balances, pay promptly or initially eliminate smaller debts to experience success versus attacking “big ones.” Shop interest rates and “carefully” transfer debt balances to other credit cards with enticing offers. Stockbrokers may counsel against being debt-free and suggest placing all your assets in the market. What a relief to know you aren’t obligated to anyone, can live comfortably, and withstand most financial storms!

Delay social security: Economists warn that in nine years, the system will take in less contributions than it sends to retirees. People are living longer and more are drawing benefits. Fewer employees are paying into the system which is rapidly draining reserves. Politicians, who focus solely on their re-election careers, refuse to support creating a stable, secure system for fear of political backlash. Studies verify monthly benefits will be reduced by 23% beginning in 2034. Significant measures being suggested by the Social Security Trustees exclude existing retirees and those 50+ years old.

Your monthly check increases 8% every year you wait to draw your retirement—almost doubling at age 70. If you haven’t applied and have adequate savings or plan to work longer, strive for the highest check you can secure!

Homes: If planning to buy real estate, markets are scarce but may improve since interest rates could decline later in 2024. Families spend 30% of their monthly income on housing. Long-term, to save money and interest, pay extra towards your monthly mortgage’s principal. Buying energy-efficient appliances, such as high-SEER heating and air equipment (HVAC), are worthy up-front investments. Unfortunately, foreign-made appliances, using cheap parts in washers and dryers, often experience major equipment problems. Purchase long-term, inexpensive warranties since moving parts will break, resulting in higher after-purchase costs! While initially expensive, US-Made Speed Queen home-commercial washers/dryers with 20+ year lifespans and seven-year parts/labor warranties are excellent!

Home utilities consume 10% of budgets. Install R-38 attic insulation to reduce energy consumption which increases re-sale values. Programmable thermostats save money and improve sleep during cooler months. If you’re a utility-cooperative member, like Mid-Carolina Electric, avoid using major appliances, such as clothes dryers, during high-demand times (6 cents per kilowatt hour off-peak versus $12.00 KWH at peak hours).

To reduce harmful dust and allergens, select high-MERV-14+ HVAC filters from Amazon and change them regularly to reduce energy. Install HVAC germ-killing-UV lights that create healthier interior air. Use energy-efficient, white-light bulbs to save and brighten homes.

Purchase service maintenance agreements from HVAC businesses to maximize efficiency. These partnerships provide priority during emergencies. Many family-owned companies have been purchased by out-of-state, profit-driven-large businesses. Use caution with commission-based HVAC staff who are pressured to sell services you don’t need—always ask for senior service technicians.

For serious home projects, outline your desires, inquire with friends about proven, quality vendors, and patiently secure bids to avoid nightmares! Learn tips from expert contractors while saving money. When project details are finalized: (1)-select reputable professionals who may match lower bids; (2)-sign written agreements containing exact project details and expectations; (3)-state payment schedules and specifically what needs to be completed for workers to receive payments (never pay upfront or prematurely); and (4)-make final settlements when all work is satisfactorily completed. Utilize credit cards, without vendor fees, which provide you with more rights—obtain detailed receipts if paying with cash/checks.

Automobiles: The second-largest family-spending category is transportation (about $10,000 annually of the average family’s income). Car and Driver Magazine reports, “New vehicles lose 20+ percent of their original value in the first twelve months—$50,000 SUVs are worth less than $40,000 a year later.” Custom-tailor your desired brands/models by visiting manufacturers’ websites to examine cars’ colors, options, and specifications. The Wall Street Journal recommends gasoline-hybrid engines which cost $1,500 extra but increase resale value, provide higher horsepower and achieve very-high gas mileage (Toyota RAV4 SUV generates 41 city-mpg).

E-mail your various selections to large-volume Internet sales reps who provide the best deals. We recently had successful experiences with Tatum Macomson (Mark Ficken Ford/Lincoln dealership in Charlotte, NC)! Avoid providing telephone numbers, rather communicate by e-mail to avoid verbal, undocumented conversations. Online efforts bypass stressful on-site sales force. Research manufacturers’ low-interest and returning customer specials. Avoid hidden fees by requesting bottom-line “out-the-door costs.” Solicit manufacturers’ window stickers which lists options. Carefully examine sales paperwork at home in advance prior to signing. Avoid being lured into attractive low monthly payments on long-term loans with high-interest rates!

Car warranties have improved with longer time periods. Thus, expensive, extended versions may be an unnecessary expense. Avoid trading cars for lower prices with dealerships. Determine your car’s retail or trade-in-value using websites like www.kbb.com. Have automobiles cleaned and detailed ($200)—post plenty of attractive inside and outside photos when advertising on Facebook Marketing, eBay, and Craig’s list. We experienced remarkable success selling cars using these sources.

Non-profit Consumer Reports (CR) recommends purchasing slightly used automobiles 2-5 years old (20,000 miles or less) with warranties to avoid hidden headaches. They experience slower depreciation, decreased loan payments, and lower taxes/insurance—CarMax.com provides used cars’ histories online and has 200 stores that buy/sell automobiles. Read CR’s automobile independent reviews of cars’ reliability and customer satisfaction.

Retain your car’s maintenance documentation for buyers. Ensure tire air pressure is correct which increases miles-per-gallon and reduces tire wear (specs are on interior driver-side door panels). Modern lubricants allow oil change intervals around 7,500 versus 3,000 miles. Because gasoline is a major car expense, seek low-cost gas stations (Cosco, Murphy, and Racetrack) and orderly plan your driving trips to conserve.

Regretfully, automobile service shops often pay their staff based on repairs, some of which you don’t need! Select honest, competent mechanics to maintain your car and examine your proposed purchases. Macky Monts with Love Chevrolet is an excellent, trustworthy service supervisor for most car brands.

Foods: Groceries and eating out consume 20% of household spending. Some prices have stabilized though we’re getting less and paying more! Register with store membership programs to receive discounts, sales alerts, and gasoline savings. Your selected online account coupons materialize when checking out. Fewer stores mail advertisements so visit them online or in person. Some offer 5% senior discount days and “Buy-One-Get-One-Free” specials. Purchase low-cost freezers to stockpile food when deals surface. Never visit stores hungry (or with children) and prepare advanced lists with pricing. Consider coupon apps like Ibotta, Fetch, and shopmium. While costs vary amongst grocery chains, Walmart, Food Lion, and Aldi are lower—knowing your prices is important.

Purchase restaurant gift cards when discounted 15-20% sales appear. Register with your favorite eateries to generate points and alerts. Food chains run happy hours, early bird pricing, and specials (Bonefish Grill occasionally offers two-person meals ($48 total), Chapin Chophouse promotes $29 weekday juicy-steak bargains, and Outback advertises $17 three-course-selections).

Automobile and Home Insurance zaps 20% of household costs. Rates are based on multiple variables, so independent agents can compare different companies’ deals. Scott Mosely of Irmo Insurance reported families often don’t communicate items that reduce premiums: monitored security systems, new roofs, youthful drivers’ academic B-averages, driver training documentation, pleasure driving, retirements, and no mortgages. Your car’s VIN number generates safety discounts but double-check policies. Paying entire bills upfront and raising deductibles to $1,000 saves money. High credit scores (750+) play into favorable-rate formulas. Visit www.AnnualCreditReport.com for free reports. Credit bureaus provide ways to improve ratings and we strongly suggest locking accounts to prevent thieves’ access. Some insurers allocate lower rates if you install cellphone apps that track driving patterns. Use caution about joining since they may miscalculate good drivers. Our next article will share stunning information on how our satellite-connected cars transmit detailed personal driving habits, like speeding, and are sold to insurance companies which can damage your ratings!

Health expenses consume 5-10% of families’ income. Maintain relationships with “lower-insurance-in-network” medical practices (preferably internists and multiple family practitioners), dentists, and specialists since your past is documented. Annual examinations can detect potential health threats. Our bodies talk to us through problem symptoms that alert us troubles are brewing (which can result in saving money). For example, if your tooth hurts, $200 dental fillings beats $3,000 root canals. If you have large medical bills, inquire if you pay entire bills to obtain a 15% discount. This often works if you wait for overdue billings and most offer payment plans. Ask doctors and pharmacists for generic medications, discount coupons, samples, and saving alternatives. Pharmaceutical companies offer name-brand lower-cost programs and free medicines for families with limited income. Type into your Internet browser “Discount programs for ‘Your Drug’s Name’ to identify legitimate sources. Medicare provides prescription low-income assistance www.medicare.gov/basics/costs/help/medicare-savings-programs.

Clothing accounts for 5% of budgets. While selections dwindle, buying winter clothes off-season in February and summer items during the fall results in 50-65% off retail prices. When sales appear, buy items before needed to reduce stress. You’ll be surprised with consignment shop and Goodwill bargains, sometimes including original tags. Some families share children’s clothes.

Internet, Cellphones, and Streaming Services devour $4,000+ per year from families. Review bills to assess reducing services and compare competitors’ pricing. Some unused streaming subscriptions sit idle with automatic billings after trials end. Educators and military often receive discounts.

Miscellaneous, Personal, and Entertainment gobble 20% of budgets—daily Starbucks’ coffee can total $1,200 annually! These little expenditures, when combined, skyrocket into BIG problems unless budgeted, tracked, and limited.

Travel and Vacations can “Wallop your wallet!” Disney four-day-family vacations average $3,500! It’s important for families to get away and have fun, especially if relaxing, but escapes can throw households into debt! Broad suggestions are: (1) Schedule trips 6-12 months ahead since prices escalate as departure times near and travel off-season to lower costs; (2) Avoid exotic, stressful vacations with children and grandchildren that require expensive airplane tickets, hotels, and meals unless you have abundant resources; (3) Plan around your time zone. Vacations in tropical Key West, Florida are less expensive than visiting Hawaii; (4) If you’re planning overseas trips, Viking cruises, with free flights, are excellent; (4) Avoid economical, stressful bus tours with constant packing/unpacking, running from one hotel to another; (5) Join free travel programs (Delta Airlines, Marriott, Hyatt, and Hilton hotels). Surprisingly, Holiday Inns provide premier European lodging; (6) Enroll with AARP and AAA which provide 15% travel discounts. After traveling 2 million miles worldwide, we published many travel tips, fun-destination articles, and saving strategies. Select “Travel” on our non-profit website for details.

Paying with cash and being debt-free are sensible approaches to saving money. Before credit cards, if you lacked cash, you didn’t buy it. However, unless you secure credit lines, your FICO credit score declines which could increase automobile/home insurance! Thus, having low-no-fee credit cards makes sense if you promptly pay them off. Apply for those that match your lifestyle. Some companies offer 2% rebates on purchases plus no annual fees (Wells Fargo Active Cash). Delta Airlines, American Express, and hotel chains such as Marriott offer sign-up points, discounts, and free travel. Thus, invest your money to generate positive results! Use caution in canceling credit cards that lower FICO credit scores—ask annual fees to be waived to keep cards.

Match-Pricing is not advertised but is often provided by retailers and banks with competitors. If you’re taking project bids, ask quality vendors to lower costs to align with the competition. Employer-retirement-matching programs are excellent ways to save!

Meet with Certified Financial Planners (CFP) who analyze your spending and guide your financial decisions. Seek experienced professionals who charge by the hour and aren’t commission-fee-based. Inquire with friends who utilize financial experts and interview consultants before engaging.

Saving can be difficult but is needed for unexpected expenses and retirement. Financial advisors recommend saving 15% of your net annual income. If invested in mutual funds, you could be a millionaire in 20 years. A modest-saving-formula—depositing $500 monthly for 20 years generates $220,000! If you have extra cash, invest in flexible-high-interest savings (Discover, Ally, or American Express Banks offer 4.3% yields). Interest costs will decline later in 2024, so seek FDIC-insured 2-3-year CDs with 4.75% rates soon.

Create budgets: To help you or your business create budgets, we have designed several options:

- An Excel spreadsheet that you can download. We have included the main budget categories and formulas for income and expenses. If you don’t need a certain listing, you can erase it and add your own topic. When you add numbers to each month, Excel will automatically total each category for the year.

- If you do not have Microsoft Excel, you can click on the budget in a PDF format, print it, and then manually insert and total your figures using an adding machine.

- A Google Budget format that, like Excel, can be downloaded and will automatically add your figures.

By creating budgets and then comparing your expenses and income to what you projected will help guide you in your spending and improve savings.

The Bottom Line: Saving money is fun while creating benefits like financial security, comfortable retirements, and peace of mind! Remember—small savings add up!

©Copyright April 2024 All Rights Reserved Mike DuBose. Please share our article by providing individuals with our website link www.mikedubose.com with the author’s credits without altering the document’s content. Our purpose is to “Create opportunities to improve lives” and we appreciate your being a partner in helping others.

Write to Mike at mike@grantexperts.com. Visit his nonprofit website www.mikedubose.com and register to receive his monthly articles or Daily Thoughts plus free access to his books, including “The Art of Building Great Businesses.” The website includes 100+ published articles he has written on business, travel, and personal topics, in addition to health research with Surb Guram, MD and our beloved pets with David Hurst, DMV.